![]() In the first two articles of this Beginner’s Guide to Investing series, we looked at some fundamental building blocks for investing:

In the first two articles of this Beginner’s Guide to Investing series, we looked at some fundamental building blocks for investing:

- Establish a reserve fund for emergencies and pay off your credit cards.

- Determine how much time you want to spend monitoring your investments, when you will need the money, and how much risk you can live with.

Here’s something that might surprise you: most millionaires in the U.S. are everyday people who followed simple guidelines for saving, spending, and investing (for more on this, check out The Millionaire Next Door by Thomas Stanley and William Danko).

Generally, U.S. millionaires do not come into their wealth through inheritance, nor by winning the lottery or beating the house at Las Vegas, nor by picking that one truly outstanding stock investment. Instead they accumulate wealth methodically and gradually by consistently investing over the duration of their career.

You may be thinking, “There’s no way I can save ONE MILLION dollars!” But could you invest $1000 a year for 50 years? With time and favorable markets on your side, that’s all it takes to become a millionaire.

You Can Create Wealth by Investing

You Can Create Wealth by Investing

Let’s say you could find an investment that generates a 10% return each year, and you invest $1,000 each year. After 50 years you will have put in $50,000. Would it surprise you to know that your investment would have grown to … over $1 million? Let’s walk through the mechanics of this.

- Start: You invest your first $1000.

- After 1 Year: You earn 10%, or $100 of income. Invest another $1000. Total is now $2100.

- After 2 Years: You earn another $210 in income. Invest another $1000. Total is now $3310.

- At the end of 10 years, you will have $17,531 in your account.

- And at the end of 50 years, you will have accumulated $1.28 million.

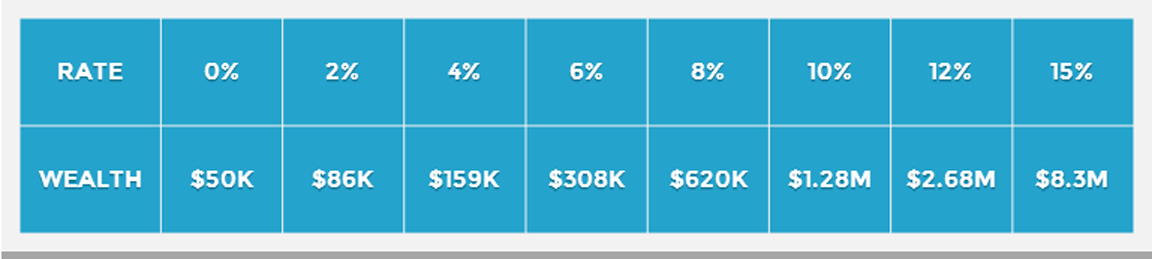

The table below shows how much wealth accumulates, at various rates of return, if you save $1,000 per year for 50 years.

The rate of return you achieve greatly affects the amount of wealth you have at the end of 50 years. Small increases make a huge difference: in our example, increasing return from 6% to 8% doubles your wealth, and moving from 8% to 10% doubles it again.

According to Morningstar, from 1926 to 2013, stocks achieved a compound annual return of 10.1%, and bonds achieved 5.5%. If the future is similar to the past, then investing $1,000 per year for 50 years at a 5.5% bond-like return would generate about 1/4 million dollars. But investing at a 10% stock-like return generates $1.28 million, or about 5 times as much! Are you starting to see why investors like stocks so much?

Start NOW!

Start NOW!

A second factor that greatly affects accumulated wealth is the number of years you allow for your investment to grow. The table below shows how much wealth accumulates, for various numbers of years, if you save $1,000 per year and earn a 10% return.

If you start now, and invest $1,000 for 50 years, you will accumulate $1.28 million. But if you wait 10 years to begin, and invest $1,000 for only 40 years, you will accumulate less than half as much!

It is possible, as many millionaires will attest, to accumulate significant wealth if you will do three things:

- Consistently and steadily set aside money for investment.

- Choose investments with higher long-term returns, as long as you can tolerate the risk.

- Begin NOW! A delay of even a few years can substantially reduce your eventual wealth.

About the Author

With a BS degree in geophysics, I took a job exploring for oil for a major energy company. I was able to save money, but knew absolutely NOTHING about how to invest it. Didn’t know what a stock was, how the price was set, how to buy a share, etc. So … I headed back to school part time—primarily to learn about stocks and bonds—and eventually earned an MBA in finance (which the oil company put to great use).

With a BS degree in geophysics, I took a job exploring for oil for a major energy company. I was able to save money, but knew absolutely NOTHING about how to invest it. Didn’t know what a stock was, how the price was set, how to buy a share, etc. So … I headed back to school part time—primarily to learn about stocks and bonds—and eventually earned an MBA in finance (which the oil company put to great use).

I’ve maintained a continued personal interest in investing, and read some outstanding books that have helped refine my investing strategy and goals over the last three decades. I’ve been with Leggett & Platt since 2000, where my professional responsibilities now include strategy, investor relations, financial communications, and analysis. But for 13 years I’ve also served as Chair of the Investment Committee that oversees our pension and 401k investments. Given that latter job role, employees sometimes ask me how they might start investing. These brief articles explain one approach that novice investors might take.

The opinions expressed by contributors are theirs alone, and do not reflect the opinions of Leggett & Platt (full disclaimer).