![]() In my first article in this series, we looked at two simple pre-investing steps to take. Before you begin investing, you must also answer these three questions:

In my first article in this series, we looked at two simple pre-investing steps to take. Before you begin investing, you must also answer these three questions:

- How much are you willing to work on monitoring investments?

- When will you need the money?

- How much risk can you live with?

1. Work Level

1. Work Level

How much time and effort you plan to devote to investing determines what type of investments you should be considering. Here are some alternatives:

Individual Stocks. If you plan to select individual stocks for your portfolio, realize that picking and monitoring individual stocks takes a consistent, significant investment of time. You’ll need to stay up on the news regarding companies you invest in, determine what additional stocks warrant inclusion in your portfolio, and determine when it’s time to sell. Plan to spend at least several hours per week overseeing your portfolio.

Active Mutual Funds. Managers of active mutual funds make the stock selections for you. Your job becomes to identify a good mutual fund manager who consistently produces strong investment returns that justify the fees they charge to select stocks for you. If you go this route, try to spend at least one Saturday morning per month reviewing the performance of your mutual funds, and determining when it’s time to pull your money out of one fund and put it into another.

Passive Index Mutual Funds. Passive index funds don’t pick individual stocks; instead, they invest in most or all stocks in their respective market. A good index fund will have low fees and will closely mimic the aggregate returns of the entire pool of investments they track. Your job becomes primarily to determine what fraction of your portfolio should be allocated to various classes of investments, e.g. large US companies, small US companies, foreign stocks, bonds, etc. On roughly an annual basis you should readjust your holdings to match your target allocation, and double check that your index funds are performing in line with the market in which they’re investing.

Target Date Funds: If you have access to target date funds (perhaps through your 401k plan) which determine for you the proper allocation to various mutual funds (based upon your age and planned date of retirement), there’s not really a lot you have to do. You should still periodically review the performance of the mutual funds in which they invest, and make sure the fees they charge are reasonable.

2. Time Frame

2. Time Frame

Basically, the sooner you need the money, the less risk you want to take with your investments.

For example, if you are saving for a need that is only two years away and you are investing in stocks, there is some meaningful chance that you will have less money in 2 years than the amount you invest, simply because stocks do go down by large amounts at times. Recall that from late 2007 through early 2009, stocks declined in value by over 50%! On average, the stock market loses money once every 3 or 4 years.

So if you are investing for the short term, your goal should be to preserve the value of your investment and not take on much risk. You might simply open a savings or money market account. But if you’re investing for a longer term goal (e.g. retirement, child’s college education), you probably want to seek the higher return (on average) that stocks offer.

Over the short term, if you invest too much in stocks, your investment could be worth less than what you put in. But over the long term, if you invest too little in stocks, your portfolio may not grow to the size you need it to be.

3. Risk Tolerance

3. Risk Tolerance

Finally, you need to understand your own level of appetite for, and comfort with, risk. Higher potential returns on your investments always come with higher risk. Money markets are safe but offer almost no return; stocks offer higher returns, but you must take the risk that comes with them.

Do you want to “sleep well,” meaning you don’t want to take the risk of losing much money? Or do you want to “eat well,” meaning you want to aggressively pursue higher returns, and can live with the risk?

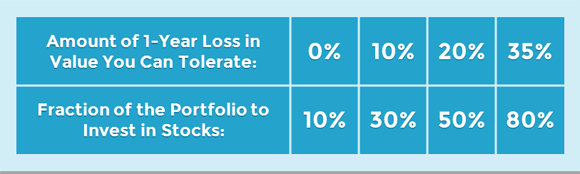

Here’s a guideline taken from the book The Intelligent Asset Allocator, that helps determine how much of your portfolio you might consider putting into stocks. You need to ask yourself this question: What is the largest one-year portfolio loss that I am willing to accept?

If you can’t tolerate the possibility of a meaningful loss, you shouldn’t invest much in stocks. Conversely, if you could live with a decline (in one year) of 1/3 the value of your portfolio, you can invest a high proportion of your portfolio in stocks.

About the Author

With a BS degree in geophysics, I took a job exploring for oil for a major energy company. I was able to save money, but knew absolutely NOTHING about how to invest it. Didn’t know what a stock was, how the price was set, how to buy a share, etc. So … I headed back to school part time—primarily to learn about stocks and bonds—and eventually earned an MBA in finance (which the oil company put to great use).

With a BS degree in geophysics, I took a job exploring for oil for a major energy company. I was able to save money, but knew absolutely NOTHING about how to invest it. Didn’t know what a stock was, how the price was set, how to buy a share, etc. So … I headed back to school part time—primarily to learn about stocks and bonds—and eventually earned an MBA in finance (which the oil company put to great use).

I’ve maintained a continued personal interest in investing, and read some outstanding books that have helped refine my investing strategy and goals over the last three decades. I’ve been with Leggett & Platt since 2000, where my professional responsibilities now include strategy, investor relations, financial communications, and analysis. But for 13 years I’ve also served as Chair of the Investment Committee that oversees our pension and 401k investments. Given that latter job role, employees sometimes ask me how they might start investing. These brief articles explain one approach that novice investors might take.

The opinions expressed by contributors are theirs alone, and do not reflect the opinions of Leggett & Platt (full disclaimer).