![]() Stocks are risky because they can be highly volatile in the short term. Individual stocks and entire markets can become “bearish”, meaning they can decline significantly in value for a period of months or even years. It’s important to fully understand that risk and appropriately manage it. I’d like to expand on my brief overview of stocks from earlier in this series by examining both the risk and reward of this type of investment.

Stocks are risky because they can be highly volatile in the short term. Individual stocks and entire markets can become “bearish”, meaning they can decline significantly in value for a period of months or even years. It’s important to fully understand that risk and appropriately manage it. I’d like to expand on my brief overview of stocks from earlier in this series by examining both the risk and reward of this type of investment.

Stock Market Risk

Stock Market Risk

The stock market continually moves up and down in value, sometimes significantly and rapidly. No one — despite what they claim — can consistently and accurately predict stock market movement.

If you’re planning to invest in stocks, it helps to know a bit about the U.S. stock market’s historical performance:

- The stock market typically posts a negative return (i.e. loses money) once every 3 or 4 years

- Annual stock returns are volatile: stocks declined 37% in 2008, but gained 32% in 2013

- From October 2007 to March 2009, the stock market lost over half of its value

- Over one and two-year periods, stocks outperform bonds only about 60% of the time

- For 2000-2009, the stock market’s compound annual return was negative 1% per year

So Why Invest in Stocks?

So Why Invest in Stocks?

Over the long term stocks offer higher returns than bonds, money markets, checking accounts, CDs, and other typical investments. Since 1926, large company stocks (in the U.S.) have achieved an annual compound return of 10%. That compares to 12% for small company stocks, only 5.5% for long-term government bonds, and 3% for inflation.[1] Investors require higher return from stocks because of the stock market’s significant short-term volatility.

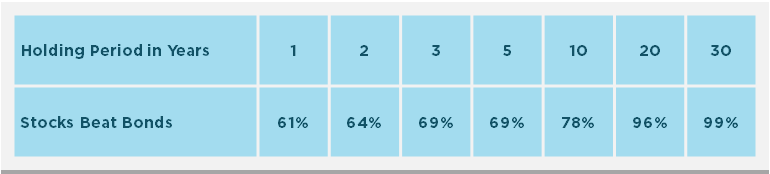

Professor Jeremy Siegel has done a lot of work to investigate the performance of stocks and bonds over the last 200 years.[2] He notes that as the investment period lengthens, the probability that stocks outperform bonds increases. The table below shows the percentage of times that stocks outperformed bonds, for various holding periods. For example, if you remained invested for 20 years, stock returns beat bond returns 96% of the time between 1871-2012.

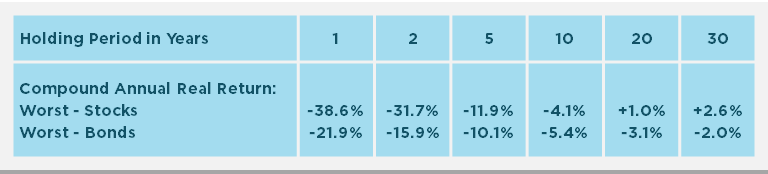

Siegel also calculates the worst performance over the last 200 years, for various holding periods. For example, the worst 20-year compound annual real return for stocks was positive 1.0%, compared to negative 3.1% for bonds.

Conclusion

Conclusion

The worst performance of stocks is better than that of bonds for investing periods of 10 years or more. In fact, between 1802 and 2012, for 20- and 30-year periods, stocks never generated negative real returns, but bonds did.

Stocks—especially over the short term—are risky. If your time horizon for investing is just a couple of years, my advice is that you stay away from stocks. There is no way you can be certain that the next 2 or 3 years won’t be abysmal for stock investors.

But over the long term, stocks are a preferred investment because:

- They offer higher returns than bonds (and money markets, CDs, etc.)

- Stocks “worst performance” is better than that of bonds

- Stocks provide a good hedge against inflation (but bonds do not)

[1] Morningstar, 2014 Ibbotson SBBI Classic Yearbook (Chicago: Morningstar, 2014), 40.

[2] Jeremy Siegel, Stocks for the Long Run, 5th edition (New York: McGraw Hill, 2014), 94-95.

About the Author

With a BS degree in geophysics, I took a job exploring for oil for a major energy company. I was able to save money, but knew absolutely NOTHING about how to invest it. Didn’t know what a stock was, how the price was set, how to buy a share, etc. So … I headed back to school part time—primarily to learn about stocks and bonds—and eventually earned an MBA in finance (which the oil company put to great use).

With a BS degree in geophysics, I took a job exploring for oil for a major energy company. I was able to save money, but knew absolutely NOTHING about how to invest it. Didn’t know what a stock was, how the price was set, how to buy a share, etc. So … I headed back to school part time—primarily to learn about stocks and bonds—and eventually earned an MBA in finance (which the oil company put to great use).

I’ve maintained a continued personal interest in investing, and read some outstanding books that have helped refine my investing strategy and goals over the last three decades. I’ve been with Leggett & Platt since 2000, where my professional responsibilities now include strategy, investor relations, financial communications, and analysis. But for 13 years I’ve also served as Chair of the Investment Committee that oversees our pension and 401k investments. Given that latter job role, employees sometimes ask me how they might start investing. These brief articles explain one approach that novice investors might take.

The opinions expressed by contributors are theirs alone, and do not reflect the opinions of Leggett & Platt (full disclaimer).